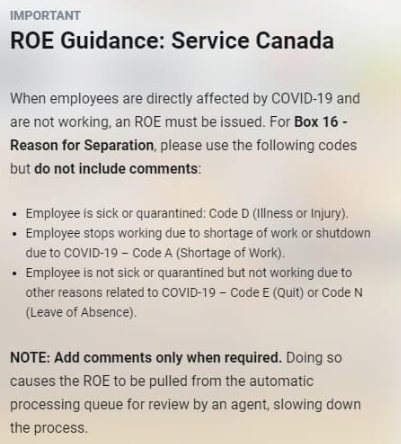

COVID-19, Change in Office Hours

Posted by Brenda Parker CPA,CGA in Uncategorized on March 22, 2020

Due to the current public health threat from COVID-19 we will be working from home for the foreseeable future. We will not be meeting with clients at our office or at home except by phone. You can send your 2019 income tax documents to us via email as scans or pictures or you can drop them off at our office in the drop box on our front counter. As you are probably aware we share our reception area with Dr. Soliman and for the time being his office will be open so you can access our counter as well. His office is open from 9-4 Monday, Tuesday and Thursday and 9-12 on Wednesday and Friday.

We have subscribed to an electronic signature service for you to sign any forms that are required by CRA or CPA Nova Scotia. We will send you pdf copies of your tax returns for you to look over before signing the e-file permission forms electronically. At the bottom of this email are the instructions that are on the drop-box on our front counter. We have been sharing the government’s financial aid responses to this situation on our Scotia Accounting Facebook page and ask you to check it out at your convenience. We hope that everyone does what is necessary to keep them and their family safe during this difficult and unprecedented time.

Stay safe,

Jim & Brenda Parker

We will be emptying our drop-off box every

Monday, Wednesday and Friday evening

Print your name on the outside of your envelope.

If you need an envelope, take one from the package next to the drop-box.

Please print your current email address and/or phone number and any notes about your 2019 taxes on one of the sheets of paper next to the drop-off box and put it in your envelope.

Changes we need to be aware of since last tax year are:

change in address, phone numbers, email address,

marital status including the date,

birth-dates of children born in 2019 or any additional dependents,

did you sell you primary residence (house) in 2019.

If you need a pen please take one from the package

next to the envelopes and take it with you after using it.

Do not leave the pen on the counter as

COVID-19 can be spread on pens.

BDC support for businesses impacted by COVID-19

Posted by Brenda Parker CPA,CGA in Uncategorized on March 22, 2020

COVID-19 Federal Government Resources for Canadian Businesses

Posted by Brenda Parker CPA,CGA in Uncategorized on March 22, 2020

CPA Canada 2018 Canadian Finance Study

Posted by Brenda Parker CPA,CGA in Uncategorized on November 15, 2018

Watch out for (and protect yourself from) these 3 sophisticated phone scams

Posted by Brenda Parker CPA,CGA in Uncategorized on November 13, 2018

There have been some breakthroughs. In recent headlines, the man behind a major lottery phone scam—with origins in Jamaica—Lavrick Willocks, was sentenced in the U.S. to six years federal prison and ordered to pay US$1.5 million in restitution. According to the FBI, there are hundreds of victims—including Canadians, and many elderly [See Seniors too ashamed to report financial fraud, say experts]—who were convinced they had won millions of dollars, and could claim their prize if they wired over a processing fee.

It’s no surprise for the Canadian Anti-Fraud Centre (CAFC). According to the CAFC, almost 22,000 complaints were received in 2017 about direct call scams with more than $21-million being reported lost. That’s up 33 per cent since 2015. And this number is likely on the low-side, as CAFC estimates that only five per cent of mass marketing fraud victims actually report the incident. [See 5 scams that took the lost money out of Canadian pockets last year]

“Regardless of where the scam is coming from, the key thing is to be on top of what scams are happening,” says RCMP Sgt. Guy Paul Larocque, acting officer in charge for CAFC. “The more you know, the better equipped you are to not follow through. Education is the best way to combat the issue.”

So how can you protect yourself? Read on for a few trending phone scams and how to avoid getting duped.

THE SCAM: CAN YOU HEAR ME?

Callers pose as service providers (think mortgage lenders or utility companies) and ask, “Can you hear me?”, shortly after the call is answered. The caller records the recipient’s response “yes” and hangs up. Jackpot! They’ve got what they need—a voice signature that can be used to authorize fraudulent charges to personal accounts and credit cards via telephone where voice authentication is permitted. (Yes, the scammer may have already obtained personal information such as credit card numbers or account information, which is used with the voice recording to authorize charges.)

The voice recording can also be used to facilitate “cramming”, a form of fraud which commonly occurs when telephone service providers permit third-party vendors to add charges to customers’ bills. As a result, the victim’s phone number is treated like a credit or debit card for the “fake” vendor. Unauthorized charges usually appear as additional features to a mobile phone or payment for services like daily horoscopes. For scammers, it’s as easy as picking an active number from a telephone directory.

The use of a voiceprint by scammers is likely to increase, say experts, with the advancement and introduction of voice biometrics software as a form of identity verification.

“Just using the technology as a new option to satisfy the customer is not enough,” says Dr. Arash Habibi Lashkari, assistant professor and R&D co-ordinator for the Canadian Institute for Cybersecurity (CIC), faculty of computer science at the University of New Brunswick. “We should think about the security as well, which is one of the main issues.” [See When choosing AI, think of the client’s privacy first, says expert Chantal Bernier]

FRAUD PREVENTION TIPS:

- Don’t answer any calls from unknown numbers. Let it go to voicemail.

- If you do answer the call, do not respond to any questions asked by a recorded voice, or a live voice. If you are asked “Am I speaking with Mr. or Mrs/Ms. (insert your name) do not say “yes”, “yes, this is” or any variation of, but instead, hang up or ask who it is that is calling you? From there, be wary of saying anything further, and do not provide any personal information.

- Be vigilant about checking your bill statements to ensure there aren’t any suspicious or unknown charges.

THE SCAM: WON’T YOU BE MY NEIGHBOUR?

Using robocaller technology, scammers (from wherever they are) pick up local numbers, familiar to the victim, so they are more likely to answer the call. Once they get a live person on the phone, they try to not only coerce them into handing over personal info and funds, but to also use their number for future scams.

The victim may be placed on hold, and then redirected to a live “agent” who could pretend to be a government or legal representative demanding a payment, or perhaps a bank representative promising a lower interest rate on your credit card or mortgage, in exchange for your personal information.

Robocall technology, in general, makes it increasingly more difficult to track down a call’s origin as they can travel through various carriers and networks, while using different phone numbers each time a call is made.

“Unfortunately, we have a system with Caller ID [where] the [scammers] can create a number from your area and use it…and they can do the same with email,” says Habibi Lashkari. “Cyber criminals are working well together. They have a very good collaboration system.”

FRAUD PREVENTION TIPS:

- Don’t answer any calls from unknown numbers, even if they appear familiar. Let it go to voicemail.

- Register your phone number with the “National Do Not Contact” list to help reduce unwanted calls, such as those from telemarketers. B Try blocking the contact number on your mobile phone (Rogers, Bell, Telus offer instructions on how to do so). Alternatively, use a robocall blocking app such as Nomorobo, Hiya Caller ID and Block, RoboKiller or Truecaller.

- If you are prompted by a recording to press a button, or a taken through a list of options, don’t make a selection, simply hang up.

- Whether listening to a recording or live person, never hand over personal information, be it your full name and address or your bank account information.

THE SCAM: CALL ME BACK

This “one ring” scam entails a fraudster calling from an unknown number—which may look domestic but is actually a pay-per-call international number—and lets it ring once, or twice, before hanging up. The hope is that the curious recipient calls the number back, which in turn racks up international-call-rate fees, or related charges, onto the victim’s phone bill or account. In some cases, it can be hundreds of dollars per minute. The charges may appear on your phone bill as a premium service.

FRAUD PREVENTION TIPS:

- Don’t answer or call back any unknown calls. Let it go to voicemail.

- If the call is indeed suspicious, consider blocking the number (see options above) and reporting the incident to authorities.

To stay informed, check out the list of more common phishing scams laid out by the CAFC. If you’ve received a scam call, or believe you’ve fallen victim to one, jot down the details including the phone number, request made, information you provided and funds you sent along, and immediately report the incident to the CAFC and your financial institution or service provider.

https://www.cpacanada.ca/en/news/canada/2018-11-05-phone-scams

Come from away

Posted by Brenda Parker CPA,CGA in Uncategorized on November 13, 2018

Atlantic Canada has a new and unexpected problem: a shortage of workers. J.D. Irving has a novel solution. Meet Susan Wilson, its director of immigration.

SW: I’m one of those people who grew up in the Maritimes, left and then came back. When I returned, I got involved in recruiting in our forestry division, where we’d had a chronic shortage of workers for a long time. We looked to countries with similar skill sets in mechanized forestry: Ukraine, Romania, Eastern Europe. So it started there, but it became obvious this was a growing challenge across the company.

Where specifically?

SW: Forestry was the first, then in late 2016 we noticed that Sunbury, one of our trucking companies, also started to see it. It’s something that’s gradually occurred over time, due to our own growth and regional demographics and an aging workforce, especially in rural areas. We asked ourselves, should we have a centre of excellence [for international recruitment] that would bridge all the JDI businesses? We work with JDI businesses that need additional workforce pipelines and don’t have experience with recruiting internationally. If a business says, “I want to recruit IT staff from a specific country,” we answer their tactical questions, spend time developing strategies, and work with government and community partners both in finding people and settling them in our communities.

I think a lot of people might be confused about why the region with the country’s highest unemployment rates is also experiencing labour shortages. Can you shed a little light on that?

SW: It’s a good question. Our recruiting strategy is to hire Canadians first, but if we’re going outside the country it’s because we’ve got a skill or a workforce gap we just can’t address locally. There are often fewer people choosing to enter the fields that we need to hire for, like the skilled workers needed in automated forestry, or long-haul trucking. We do a lot of work in high schools and colleges, but there’s less interest among young folks in some of these fields. The generation graduating from school today is looking at those jobs and asking, “Is this attractive to me?” So we need to shift as well, looking at X number of students coming out of school and matching that with our business requirements. It’s complex because we have so many industries. Then layer over that rural and urban—a lot of our operations are rural—and it’s complex. Some people would call it a skill or desirability mismatch. It could also be a specific skill set—in Halifax’s shipyard, there may be specialized design roles, for example.

“Little things are important. there’s nothing quite like meeting someone at the airport for the first time.”

What countries are you focusing on?

SW: It’s very industry- and business-specific. We use as much data as possible to look at the workforce: which countries have the skill sets, as well as people interested in moving to Canada? I’m working with all the JDI businesses to look at what they will need in terms of manufacturing, backroom business services, IT, engineering. We then connect with recruiters, go to job fairs and so on. What we’re finding is that people will go back to their home country and refer others to us. We recently took one of our international hires back to Ukraine, and it had such an impact. [Ukrainians] don’t know us, but he told his story and how he and his family have made a home here. That was heartwarming.

Do newcomers require any additional training?

SW: We haven’t seen that. Our focus is to hire skilled workers with the experience necessary to do the job.

Historically, most immigrants to Canada go to M.T.V.—Montreal, Toronto, Vancouver. That’s begun changing in the past decade, with an increasing proportion heading to small cities. Still, it must be a challenge recruiting people to a region they know nothing about.

SW: It’s true—people don’t know where we are. When you first talk to people, they say, “I need to go to Toronto.” But when you speak to them more, you find out that, a lot of times, people are only aware of a few cities in Canada. Some people will be drawn to those cities, but a lot of people prefer a different kind of community. They just don’t know it exists here. As employers, we have to do our due diligence. What is important to people? Why are they coming? Will they be happy in a rural community or a smaller centre?

What are people asking you about when you travel overseas?

SW: Most of the questions are around lifestyle, currency and taxation, school systems. Really, they’re trying to figure out what it’s going to be like, and what it will be like for their families. We also spend a lot of time working with under-employed and unemployed people already here, and with international students at colleges and universities. They know what it’s like here already, and so many of them want to stay, but need a way to break into the labour market.

Do most of your hires end up working in small towns?

SW: It’s a mix of urban and rural, which creates different challenges. In Nova Scotia, a lot of people are in Halifax and that area, which is very different for a newcomer than a small community in central New Brunswick, where there aren’t the same services, multicultural associations or established immigrant communities. But as these communities grow—and they really have in the past few years—we have to make sure that we’re connecting people coming in with those existing communities.

“For international hires, especially, we go above and beyond to ensure they have a buddy in their workplace they can contact.”

How do you do that? What kind of on-the-ground package do you provide for newcomers?

SW: Family and household support is the key. We have a customized settlement plan for each family, which might mean, in the first few days, supporting them by answering questions like “Where’s the grocery store?” or pointing them to the activities they’re used to in their country, or addressing their children’s needs in terms of school. It’s also really important to have a single point of contact on our end—a person they can call with questions about Canada, New Brunswick, Nova Scotia, wherever they are. For international hires, especially, we go above and beyond to ensure they have a buddy in their workplace they can contact, and we take pains to connect them with existing employees from their home country or community.

Little things are important too. We greet people at the airport with a gift basket, which is something we’re working on upgrading. Honestly, there’s nothing quite like meeting someone at the airport for the first time. Of course, we’re talking about the workforce, demographics and the health of the regional economy, but it’s ultimately about people.

Recent public-opinion polls show that Canadians are now slightly less favourable to immigration than they have been in the past. Are you experiencing any pushback to what you’re doing, especially in smaller communities where residents might not be used to newcomers?

SW: This spring, we participated in a tour of 15 cities in New Brunswick led by the New Brunswick Multicultural Council. We were out there to educate folks who haven’t had that much exposure to newcomers about the need for immigration to drive prosperity and address population challenges. That might open people’s eyes to what not having more immigration could mean for services and tax revenues. That approach is a good start in terms of helping people understand the facts. The number one topic is the economic health of the community. It’s still too early to tell what the long-term economic impact will be. I think that might be best left to economists and politicians at the local level to gauge.

The other thing that came through in the rural discussions were local business people who didn’t have any succession plan, and they were looking for that, and were open to newcomers being part of that.

So you didn’t hear much resistance to the idea of immigration in itself as way of growing the population or workforce?

SW: I can’t speak for everyone in those communities, but it’s not something we heard.

You’ve only been doing this particular job a few months, but what are the early results?

SW: In terms of progress versus our 2018 target to hire more than 200 newcomers, we are trending to fall short, and will be continuing to look to fill those openings as we move into 2019. It is hard to say currently how many people we will bring in via immigration in 2018, as many are still working through the immigration process now.

One story comes to mind. A couple of years ago, when we started doing international recruitment in forestry, we hired a man from Ukraine, just a wonderful person. After working with us, he got his permanent residency and started his own forestry business. So he’s now a small-business owner in New Brunswick and has hired people to come work for him from his country. We’re really aiming for long-term retention. And when people come here, settle their families, integrate into communities, and then become ambassadors back in their own country, it’s just amazing.

https://www.cpacanada.ca/en/news/pivot-magazine/2018-11-07-come-from-away

Home Buyers’ Plan (HBP)

Posted by Brenda Parker CPA,CGA in Uncategorized on March 11, 2015

The Home Buyers’ Plan (HBP) is a program that allows you to withdraw funds from your registered retirement savings plans (RRSPs) to buy or build a qualifying home for yourself or for a related person with a disability. You can withdraw up to $25,000 in a calendar year.

Generally, you have to repay all withdrawals to your RRSPs within a period of no more than 15 years. You will have to repay an amount to your RRSPs each year until your HBP balance is zero. If you do not repay the amount due for a year, it will have to be included in your income for that year.

Conditions for HBP eligibility and RRSP withdrawals

HBP eligibility conditions

To be eligible:

- you must be considered a first-time home buyer;

- you must enter into a written agreement to buy or build a qualifying home for yourself, for a related person with a disability, or to help a related person with a disability buy or build a qualifying home. Obtaining a pre-approved mortgage does not satisfy this condition;

- you must intend to occupy the qualifying home as your principal place of residence no later than one year after buying or building it. If you buy or build a qualifying home for a related person with a disability, or help a related person with a disability buy or build a qualifying home, you must intend that that person occupy the qualifying home as his or her principal place of residence; and

- in all cases, your repayable HBP balance on January 1 of the year of the withdrawal must be zero.

Notes

You are responsible for making sure that all HBP conditions are met.

Even if you or your spouse or common-law partner has previously owned a home, you may still be considered a first-time home buyer.

If you do not meet the conditions to participate in the HBP in the current year, you may be able to participate at a later year.

RRSP withdrawal conditions under the HBP

- You have to be a resident of Canada at the time of the withdrawal.

- You have to receive all withdrawals in the same calendar year.

- You cannot withdraw more than $25,000.

- Only the individual who is entitled to receive payments from the RRSP (the annuitant) can withdraw funds from an RRSP. You can make withdrawals from more than one RRSP as long as you are the annuitant (plan owner) of each RRSP. Your RRSP issuer will not withhold tax on these amounts.

- Generally, you will not be allowed to withdraw funds from a locked-in RRSP or a group RRSP.

- Your RRSP contributions must remain in the RRSP for at least 90 days before you can withdraw them under the HBP, or the contributions may not be deductible for any year.

- If you are withdrawing funds from your RRSPs to help a related person with a disability buy or build a qualifying home, it is the related person with a disability who must have entered into such an agreement.

- Neither you nor your spouse or common-law partner or the related person with a disability that you buy or build the qualifying home for can own the qualifying home more than 30 days before the withdrawal is made.

- You have to buy or build the qualifying home for yourself, for a related person with a disability, or to help a related person with a disability buy or build a qualifying home before October 1 of the year after the year of the withdrawal

- You have to complete Form T1036, Home Buyers’ Plan (HBP) Request to Withdraw Funds from an RRSP for each eligible withdrawal. For more information on completing the form, go to Completing Form T1036.

Note

If you make a RRSP withdrawal under the HBP and a condition is not met while you are participating in the plan, your RRSP withdrawal(s) may not be considered eligible. You will have to include part or all of the withdrawal(s) as income on your income tax return for the year you received the funds. If we have already assessed your return for that year, we will reassess it to include the withdrawal(s).

Forms and publications

Self Employed income tax deadline

Posted by Brenda Parker CPA,CGA in Uncategorized on June 3, 2014

Self-employed? If you or your spouse or common-law partner carried on a business in 2013, your return has to be filed on or before June 15th, 2014. If you have a balance owing for 2013, interest will be charged starting May 5th, 2014 at 5% per annum.